Zopa's performance during the 2007/8 recession

As I sat down to write this, the media were avidly discussing the potential of the first interest rate move in seven years -- not up as we were discussing a few months ago, but down to almost unprecedented lows. In the end, the rates were held, but the speculation reflects the mood of economic uncertainty in the UK since the vote to leave the EU.

This economic uncertainty is not unknown to Zopa. Having started lending in 2005, we are the only peer-to-peer platform to have operated through the 2007/8 recession (delivering positive returns to lenders throughout).

We therefore thought it would be a good time to take a more detailed look at Zopa's history, and delve into how we manage credit risk and deliver consistent returns to lenders. Starting with this post looking at Zopa's track record in managing credit risk through different economic environments, in the next few weeks we will go into detail about:

the wealth of data Zopa uses to make its credit models

how Safeguard works in different scenarios

our ability to respond to macroeconomic changes

Zopa's performance in 2007/8

Consistency in the face of volatility

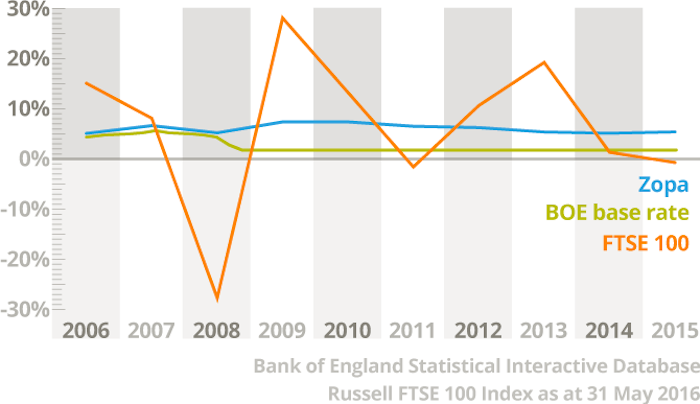

The data shows that our returns, even through the peak of the last recession, were not subject to the same volatility that the stock market suffered from. There was a slight dip in 2008 when default rates went up (see the graph below), but we still generated positive returns to our lenders.

Average annualised returns of different asset classes

Transparency -- why meeting our expected returns matters

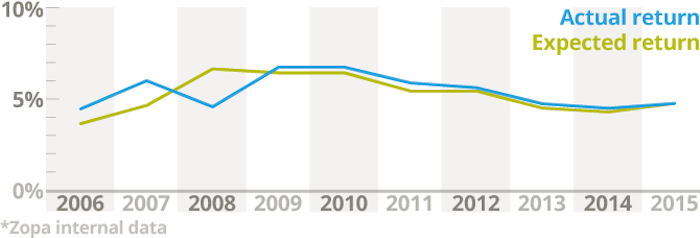

Even more importantly, our predicted lender returns performed closely to our expected returns. The only year when actual dipped below expected was in 2008, the height of the crash, and we are getting better and better at precisely hitting our expectations.

Zopa actual vs expected returns

This transparency about our returns and defaults is one of Zopa's core principles. Defaults are published on our website and our loan book, which is updated monthly, is available for anyone to download and analyse. This lets our lenders know that they can trust us and gives them a mechanism for holding us to account. We will remain committed to this.

Learning from 2007/8

We use the data from the performance of our loans throughout this period to shape our credit risk and underwriting policies. They are designed to deliver positive lender returns, even in economic conditions akin to the last crash. We'll share more detail on this soon.

In the next post, I'll look at the data we've gathered in the last eleven years and how we use it to make these decisions.

Sharvan Selvam is Head of Risk at Zopa.